In the wake of the mass movement against anti-Black racism that arose in 2020 following the police murders of Breonna Taylor, George Floyd, and countless others, both foundations and corporations have pledged to make amends by investing in Black businesses. According to McKinsey & Company, collectively the nation’s leading 1,000 corporations pledged $200 billion. Even if much of that money is simply a relabeling of pre-existing dollars, at least some of it represents new investment.

Hopefully, these investments will have some positive impact, but history encourages us to be cautious. A significant portion of recent investors in Black businesses take Black capitalism as their operating theory—that is, they assume that the path to racial equality is paved with Black business success. If racism has left Black Americans with less capital than white Americans, then the solution is to help Black Americans eventually own businesses as large and profitable as those of white Americans.

Capitalism, in this conception, is “race neutral”—business is business. According to this point of view, to achieve racial justice, the existing economic system does not need to fundamentally change. The problem is simply one of shifting ownership and control of the economic system so that such ownership and control is not enjoyed by predominantly white people but is instead equitably distributed across races.

The appeal of Black faces in high places is undeniable. And certainly no one would argue that representation is unimportant. Nonetheless, such a simple formulation misses a lot, including the fact that such investment practices have been tried before—and failed many times before. The notion of Black capitalism has a long pedigree. It appeared in some of the writings of Booker T. Washington from the 1890s and became US federal policy during President Richard Nixon’s administration.

Why did these approaches fail? There are many reasons, but the work of the late Black political scientist, Cedric Robinson, offers a particularly cogent explanation. In his book, Black Marxism, published in the early 1980s, Robinson contended that we should think of the global economic system not merely as “capitalism” but as “racial capitalism,” arguing that racism is not a “bug” of the global capitalist economy. Rather, racism is a core part of capitalism’s DNA.

The Enduring Appeal of Black Capitalism

The US has a long and bloody history of racial terrorism targeting Black-owned businesses. This history includes the racist pogrom that destroyed Tulsa’s “Black Wall Street” in 1921, which was widely commemorated last year during its centennial. The implication of these memorials was that, without the ever-present specter of racist violence that characterized Jim Crow, Black Americans would have similar levels of income and wealth to white Americans today.

Promoting Black capitalism has been the preferred approach of both major political parties since Nixon unveiled a program of tax incentives for Black businesses in an effort to head off more militant alternatives. For a nation that venerates entrepreneurship and deifies business leaders, this vision holds great attraction. As Mehrsa Baradaran, author of The Color of Money: Black Banks and the Racial Wealth Gap, outlines in the New York Times, “Black capitalism was so politically appealing, every administration since Mr. Nixon’s has adopted it in some form. Black capitalism morphed into Ronald Reagan’s ‘enterprise zone’ policy, Bill Clinton’s ‘new market tax credits,’ and Barack Obama’s ‘promise zones.’” Donald Trump’s 2017 Tax Cuts and Jobs Act also included similar “opportunity zones.”

Black Capitalism’s Shortfalls

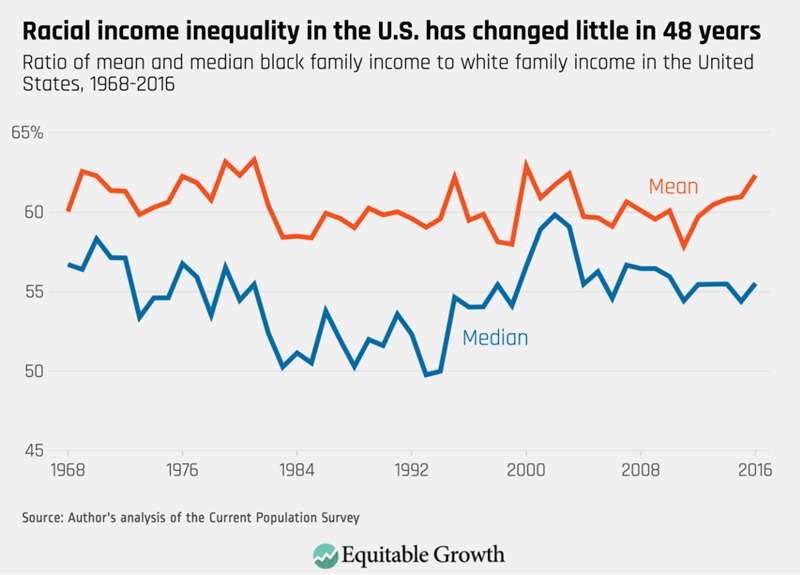

Despite repeated promises by US presidential administrations since 1970 to kickstart Black capitalism, it has failed to take-off, and racial income and wealth gaps have remained frustratingly persistent. Research by the Washington Center for Equitable Growth, a progressive think tank, shows that racial income inequality has changed little since the civil rights movement. The median income of Black households has hovered at around 55 percent of that of white households since 1968, while the average income of Black households has been about 60 percent of white households.

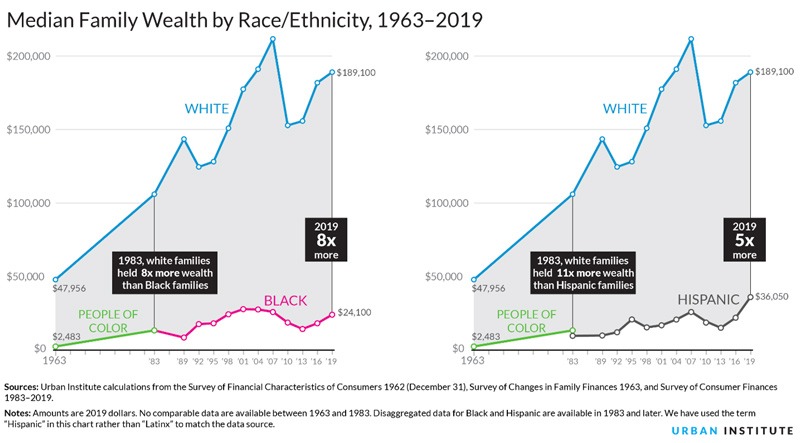

William “Sandy” Darity and Darrick Hamilton—two leading economists studying racial inequality, along with a host of other colleagues—assert in a 2018 paper that the racial wealth gap is the best measure of the burden that historic and ongoing racism has imposed on Black Americans. The Urban Institute reports that in 1983, the median white family had eight times the wealth of the median Black family. In 2019, the gap was the same!

Black Americans make up 13 percent of the population but own an estimated 2.6 percent of US wealth. Households that fall within the top one percent of wealthiest Americans are 96.1 percent white and only 1.4 percent Black. As a research team led by Darity wrote, Federal Reserve data from 2016 indicate that to be in the top one percent of wealthiest white Americans, you need $12 million in net worth, while a measly $1.574 million gets you into the Black one-percent club. Why have decades of official support for Black capitalism failed to close the racial wealth gap?

Capitalism and Inequality

One possible explanation is the “Piketty principle,” named after the French economist, Thomas Piketty, who documented rising concentrations of wealth in his magnum opus, Capital in the 21st Century. Piketty famously argues that the rate of return on capital has been higher than the rate of overall economic growth in most rich countries for most of their history. If capital returns—profits, dividends, interest, and rents—rise faster than overall incomes, then high and rising wealth inequality is inevitable.

Piketty demonstrates that reductions in wealth inequality are exceptional, the result of political intervention. Wealth inequality in Western Europe fell when the world wars destroyed the fortunes of many rich Europeans. Social democratic reform in the wake of World War II—especially progressive taxation and high levels of unionization—also contained wealth inequality. The rise of neoliberalism since the 1980s, however, has once again caused income from property to grow much faster than overall income, leading to today’s extreme levels of wealth and income inequality.

If large fortunes grow faster than smaller ones and white Americans start with more wealth than Black Americans, it follows that the racial wealth gap will be stagnant at best and, at worst, will increase over time. “Free markets” left to their own devices will never close the racial wealth gap. As Darity et al, explain, “Blacks cannot close the racial wealth gap by changing their individual behavior—i.e., by assuming more ‘personal responsibility’ or acquiring the portfolio management insights associated with ‘financial literacy’—if the structural sources of racial inequality remain unchanged.” There are simply “no actions that black Americans can take unilaterally that will have much of an effect on reducing the racial wealth gap.” Black capitalism with its emphasis on individual action is unlikely to succeed. As Baradaran concludes in her New York Times op-ed: “If the rollout of the Black capitalism program had demonstrated anything, it was that economic power could not be achieved without government help.”

Can Racial Capitalism Be Reformed?

Even if it were possible for Black wealth to grow faster than white wealth despite the headwinds identified by Piketty, it would still take unbearably long. Last year, Ellora Derenoncourt, an economist at Princeton University, and three colleagues at German universities released preliminary research that examined the evolution of the racial wealth gap since the end of the US Civil War. The paper’s authors estimate that even if Black and white wealth grew at the same rate—that is, with equal capital gains, rates of return, and savings rates, all unlikely outcomes of a system where having money helps generate more money—it would take over 200 years to close the racial wealth gap (2). Using more realistic assumptions that project forward the economic patterns of the past 50 years, the authors add that the answer to when the racial wealth gap will close, “strikingly, is never” (15).

In response to these dire predictions, Hamilton has proposed that the federal government provide each child that does not already have a trust fund with such a fund upon birth. Children born to families with the least wealth would get the biggest endowments, up to $60,000. When they turn 18, account holders could access the funds for investment—to pay for college, buy a home, or start a business. While this would certainly make a significant dent in the racial wealth gap, it does not directly address the Piketty principle: so long as white fortunes are growing faster than Black ones, the racial wealth gap will persist.

Darity and his coauthor, A. Kirsten Mullen, have made a more ambitious proposal advocating for reparations for Black Americans for slavery, Jim Crow, and current racial discrimination. This proposal calls for the US federal government to make direct payments, totaling $10 to $12 trillion, to each Black descendant of Africans enslaved in the US (controversially, the program would exclude Black immigrants). Putting aside whether such a proposal will ever gain majority support in Congress, would it actually close the racial wealth gap for good? While it would immediately close the wealth gap, such a proposal would not guarantee that the racial wealth inequality would not re-emerge. Again, so long as the returns to white wealth remain higher, then white wealth will eventually outpace Black wealth. The problem, as Piketty demonstrates, is that capitalism is an inequality-producing machine.

One of the threads uniting the Black radical tradition is the assertion that it is impossible to achieve racial equality in a capitalist society. For at least a century, Black Marxists like WEB DuBois, CLR James, and Claudia Jones have argued that capitalism cannot survive without racism, which allows capitalists to “divide-and-conquer” the working-classes. Emphasizing racial divisions hinders workers from organizing stronger unions, lowering the wages of both white and Black workers. Without racist ideas to justify glaring social inequalities, a capitalist social order would be a lot more unstable and susceptible to radical challenges. As historian and prison abolitionist Ruth Wilson Gilmore states bluntly, “capitalism is never not racial.”

What Do Racial and Economic Justice Require?

Even if promoting Black capitalism could close the racial wealth gap, is our vision of a just society in the US simply one where the top one percent is roughly 13 percent Black, 18 percent Latinx, six percent Asian, and 1.5 percent Native American—ie, one where the elite looks more like the mass of workers it exploits? Is massive wealth inequality justified so long as it is not racialized? Are poverty wages less miserable because your boss is Black? Is substandard housing less dangerous because your landlord is Black? Are monopoly prices any more affordable because the company is Black owned?

There is something deeply ahistorical underlying current efforts that ignore and indeed reproduce previous efforts to combat racial inequality by employing the strategies of Black capitalism as the primary path. Even if Black capitalism can ultimately “deliver” racial equality, the data suggests it would take centuries do so. Moreover, our horizon for social justice should be far more profound than simply diversifying the elite.

As long as capitalism remains an “inequality producing machine,” it will prevent racial equality. Fred Hampton, the charismatic young leader of the Chicago chapter of the Black Panther Party who was murdered by Chicago police and the FBI in 1969, explained this succinctly: “We’re not going to fight capitalism with Black capitalism, but we’re going to fight it with socialism.”

Black communities have long pursued an alternative approach to racial equality founded on collective ownership and democratic management of businesses and housing. As economist Jessica Gordon Nembhard details in her book, Collective Courage: A History of African American Thought and Practice, Black cooperatives are rooted in the mutual aid efforts of the formerly enslaved during Reconstruction. While Booker T. Washington was preaching Black capitalism, WEB DuBois published a book in 1907 titled Economic Cooperation Among Negro Americans, advocating for more Black cooperatives. Several prominent leaders of the civil rights movement, like Ella Baker and Bayard Rustin, were members of the Young Negro Cooperative League in the 1930s. Now grouped under the banner of the “solidarity economy,” these initiatives promised a more egalitarian society by directly challenging capital’s concentrated ownership.

A movement that seeks economic justice without addressing race and other forms of inequality would surely fall grossly short of the mark. But that very same observation, I contend, also applies in reverse: employing Black capitalism as the primary path for achieving racial justice is certain to disappoint. Liberation will only come if we are expansive enough in our vision to address inequality in all its forms.

![[PODCAST] Nonprofit Organization Annual Reports: Show Don’t Tell!](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_vDLEWw-5T520U3cp-QLqK3Y29STJYwESLTMDyVbbfw57TYQ4MeO8Clq9zLcav0IxekhQKT9AnsVUxV2j3fRFyuE8mNdWfEnW-yrsAu9yI4vRC38K-kX3XrZd3tYdMu-INhoUoIjZitunKeGxHZMqvs2m4P9-1aNkL5AcCxo6WREXn20t12Uw=w680)

0 Commentaires